Before you open your bank account application online, take a look at the benefits as well as the time frame involved. This will let you know which banks will allow you apply online. Continue reading to learn more about the process. This article will provide information about the documents required and the time it will take to open a bank account online. Although there are many advantages to opening an online bank account, there are also some things you need to know before you get started.

Benefits of opening a bank account online

There are many benefits to opening an online bank account. Online-only banks usually have lower fees than traditional banks and offer higher rates. The best part is that you don’t have to close your current account. It may be beneficial to have two accounts in the same bank - one for savings and one for checking. This will give you the best of both worlds, and help you save money and time. Learn how to get started.

Many people find this a significant advantage as they can access their account online 24 hours a days. With most online banks, you can check your account balances at anytime. To monitor account activity, your mobile phone can be used. Online banks also usually charge lower fees and offer more basic account features. You can check your balances anytime you like with some mobile apps. And they're often available around the clock, which is another benefit.

Documentation required

If you have a photo identification and proof of your address, you can open an online bank account. An ID card issued by the state or passport is required to open an account online. The proof of address you provide should match the name on your photo ID. Only one photo ID will be needed for each branch application. The other document must prove your address. A passport number or alien identification card can be presented if you're a foreign national.

Once you have all the documents ready, it's time to choose a bank. This can be daunting as there are so much to choose from. Once you have decided on a bank to use, you will need identification. The initial deposit to an account might also be required. You can make an initial deposit online in most cases. However, some banks will require you to submit paperwork.

Timeframe to open an online bank account

There are many factors that can affect the time frame for opening an online bank account. The application process can be completed online in less than 15 minutes. It may take several days if you are unable to complete the online application. For help if you encounter problems, please contact the customer service department of your bank. Many online banks have 24-hour customer support.

It is easy to open a bank account online with most banks. First, choose the bank or credit union that you wish to use and provide the required information. Once the formalities are over, you're able to open an account. However, it's still important to know how long the process will take. Knowing the timeline for opening an online bank account will help you prepare better for the future.

Which banks allow you open an account online?

Online banking offers many benefits, including convenience, speed, and low minimum deposits. While some online banks do not require any deposit, others may require you to make a small initial deposit. The type of account that you wish to open will determine the type of deposit you make. Some banks accept blank checks and credit cards as your first deposit. If you want to avoid any hassles, you can always transfer your money from another bank to your new online bank.

Many online banks offer various types of accounts including checking, savings, business, and money market. You can select which type you want by looking at the monthly fees and interest rates. You can even choose to open more than one bank account in one session to save time. Additionally, this will save you money on visits to the bank branch. However, many banks will require that you visit the branch in order for you to open an Account.

FAQ

Which age should I start investing?

The average person invests $2,000 annually in retirement savings. But, it's possible to save early enough to have enough money to enjoy a comfortable retirement. If you don't start now, you might not have enough when you retire.

You need to save as much as possible while you're working -- and then continue saving after you stop working.

The earlier you start, the sooner you'll reach your goals.

If you are starting to save, it is a good idea to set aside 10% of each paycheck or bonus. You may also invest in employer-based plans like 401(k)s.

Contribute at least enough to cover your expenses. You can then increase your contribution.

Can I make a 401k investment?

401Ks offer great opportunities for investment. However, they aren't available to everyone.

Most employers offer their employees two choices: leave their money in the company's plans or put it into a traditional IRA.

This means that your employer will match the amount you invest.

Taxes and penalties will be imposed on those who take out loans early.

Which fund is best suited for beginners?

The most important thing when investing is ensuring you do what you know best. FXCM is an online broker that allows you to trade forex. You can get free training and support if this is something you desire to do if it's important to learn how trading works.

If you are not confident enough to use an electronic broker, then you should look for a local branch where you can meet trader face to face. You can ask questions directly and get a better understanding of trading.

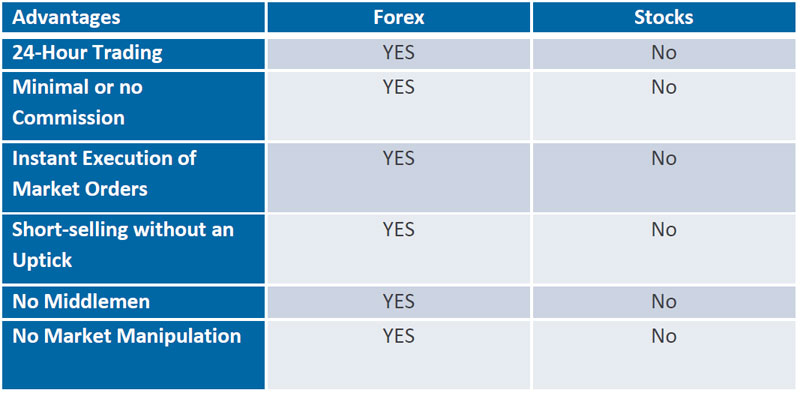

Next, you need to choose a platform where you can trade. CFD platforms and Forex trading can often be confusing for traders. Both types trading involve speculation. Forex does have some advantages over CFDs. Forex involves actual currency trading, while CFDs simply track price movements for stocks.

Forex is more reliable than CFDs in forecasting future trends.

Forex can be volatile and risky. CFDs are preferred by traders for this reason.

We recommend that Forex be your first choice, but you should get familiar with CFDs once you have.

What are the types of investments you can make?

These are the four major types of investment: equity and cash.

Debt is an obligation to pay the money back at a later date. It is commonly used to finance large projects, such building houses or factories. Equity can be defined as the purchase of shares in a business. Real estate is when you own land and buildings. Cash is what your current situation requires.

You are part owner of the company when you invest money in stocks, bonds or mutual funds. You are part of the profits and losses.

Do I invest in individual stocks or mutual funds?

The best way to diversify your portfolio is with mutual funds.

However, they aren't suitable for everyone.

For instance, you should not invest in stocks and shares if your goal is to quickly make money.

You should opt for individual stocks instead.

Individual stocks give you greater control of your investments.

In addition, you can find low-cost index funds online. These allow you track different markets without incurring high fees.

Statistics

- As a general rule of thumb, you want to aim to invest a total of 10% to 15% of your income each year for retirement — your employer match counts toward that goal. (nerdwallet.com)

- They charge a small fee for portfolio management, generally around 0.25% of your account balance. (nerdwallet.com)

- Most banks offer CDs at a return of less than 2% per year, which is not even enough to keep up with inflation. (ruleoneinvesting.com)

- If your stock drops 10% below its purchase price, you have the opportunity to sell that stock to someone else and still retain 90% of your risk capital. (investopedia.com)

External Links

How To

How to Save Money Properly To Retire Early

Planning for retirement is the process of preparing your finances so that you can live comfortably after you retire. This is when you decide how much money you will have saved by retirement age (usually 65). Also, you should consider how much money you plan to spend in retirement. This includes travel, hobbies, as well as health care costs.

You don't always have to do all the work. Financial experts can help you determine the best savings strategy for you. They'll examine your current situation and goals as well as any unique circumstances that could impact your ability to reach your goals.

There are two main types of retirement plans: traditional and Roth. Roth plans allow you put aside post-tax money while traditional retirement plans use pretax funds. Your preference will determine whether you prefer lower taxes now or later.

Traditional Retirement Plans

A traditional IRA allows you to contribute pretax income. If you're younger than 50, you can make contributions until 59 1/2 years old. If you want to contribute, you can start taking out funds. After you reach the age of 70 1/2, you cannot contribute to your account.

A pension is possible for those who have already saved. These pensions can vary depending on your location. Many employers offer matching programs where employees contribute dollar for dollar. Others provide defined benefit plans that guarantee a certain amount of monthly payments.

Roth Retirement Plans

With a Roth IRA, you pay taxes before putting money into the account. You then withdraw earnings tax-free once you reach retirement age. However, there are limitations. There are some limitations. You can't withdraw money for medical expenses.

A 401(k), another type of retirement plan, is also available. These benefits may be available through payroll deductions. Extra benefits for employees include employer match programs and payroll deductions.

401(k) Plans

Most employers offer 401(k), which are plans that allow you to save money. These plans allow you to deposit money into an account controlled by your employer. Your employer will automatically contribute a percentage of each paycheck.

You decide how the money is distributed after retirement. The money will grow over time. Many people choose to take their entire balance at one time. Others distribute their balances over the course of their lives.

You can also open other savings accounts

Some companies offer additional types of savings accounts. At TD Ameritrade, you can open a ShareBuilder Account. You can use this account to invest in stocks and ETFs as well as mutual funds. In addition, you will earn interest on all your balances.

At Ally Bank, you can open a MySavings Account. You can use this account to deposit cash checks, debit cards, credit card and cash. Then, you can transfer money between different accounts or add money from outside sources.

What To Do Next

Once you've decided on the best savings plan for you it's time you start investing. Find a reliable investment firm first. Ask friends or family members about their experiences with firms they recommend. Check out reviews online to find out more about companies.

Next, calculate how much money you should save. This step involves determining your net worth. Your net worth is your assets, such as your home, investments and retirement accounts. It also includes liabilities like debts owed to lenders.

Once you know your net worth, divide it by 25. This number is the amount of money you will need to save each month in order to reach your goal.

For example, let's say your net worth totals $100,000. If you want to retire when age 65, you will need to save $4,000 every year.